#3 - Sydney Credit Union Loan Accounts; Deconstructed

Why hide these accounts from the court? (~15 minute read)

This is my second article exposing evidence of accounting fraud by “lending” institutions in Australia, whose customers are happy for their records to be published anonymously. I‘m still focused on presenting evidence at this stage; the consequences of this evidence are yet to be discussed in detail, although it’s hard to avoid noticing the obvious implications, if you understand “The Rules”.

The Rules

Readers unfamiliar with ‘magic’ or double-entry accounting should read #1 - Bank Accounting; Magic? to brush up on my six basic rules of double-entry accounting, before proceeding. If you can’t remember these rules, what you are about to read may seem confusing. I’ve included Figure 4 from that article here for reference, and it may be helpful if your can print a copy and keep it handy as you read this (and following) articles.

The EVIDENCE

Sydney Credit Union “Loan” Accounts

Accounts featured in this article belong to a member of the Sydney Credit Union [SCU]1 in Australia (I’ll call him “Tony”) who has allowed release their contents, provided they don’t publicly identify him.

Case Details

Tony opened his account on 15 April 2014 with a $5.00 deposit and purchased a $1.00 share. On 1 May 2014, he applied for a $30,000.00 “loan” and ended up with a $29,900.00 after a $100.00 “Personal Loan Approval Fee” was taken out of his “loan funds”.

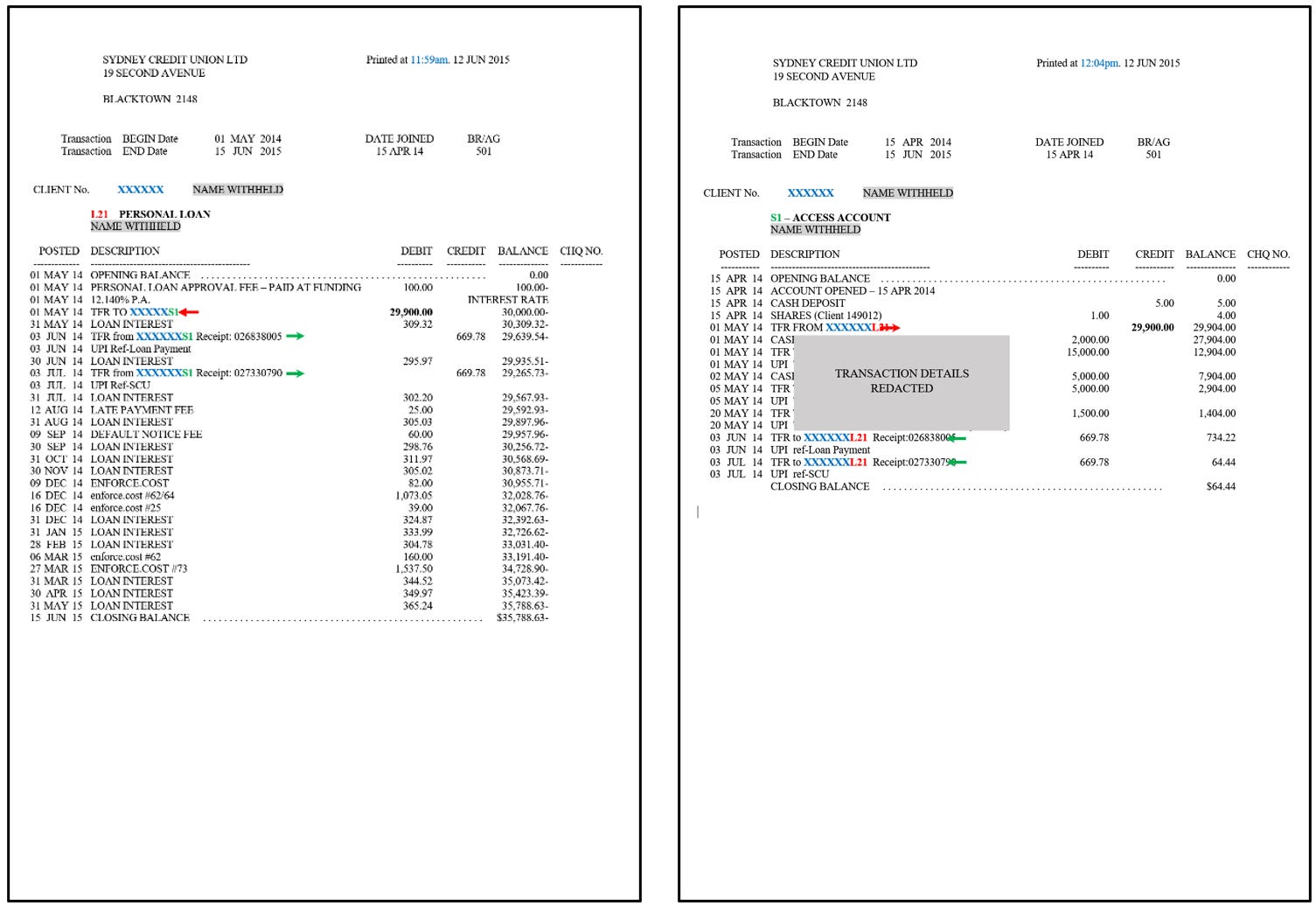

Other documents I’ve seen show that these documents were obtained under subpoena during a court case2, and Tony was only allowed to view these alone, in a closed room, under video surveillance. As Figure 1 shows, Tony took photographs of his accounts.

Account Details

As these (partly redacted) photos are hard to read, facsimiles were prepared using MS Word and independently checked for accuracy. With added colouring to assist discussion, these are shown below in Figure 2 with Client Name and some transaction details redacted and 6-digit Client No. converted to “XXXXXX” (blue).

The LH panel is titled “L21 PERSONAL LOAN” and the RH panel “S1 ACCESS ACCOUNT”.

Enlarged views of these statements (truncated, with added coloured titles, highlighting and arrows) are shown separately in Figures 3 & 4 below. The accounts can be identified as Asset and Liability accounts, respectively, using RULES 3, 4 & 5 as follows:

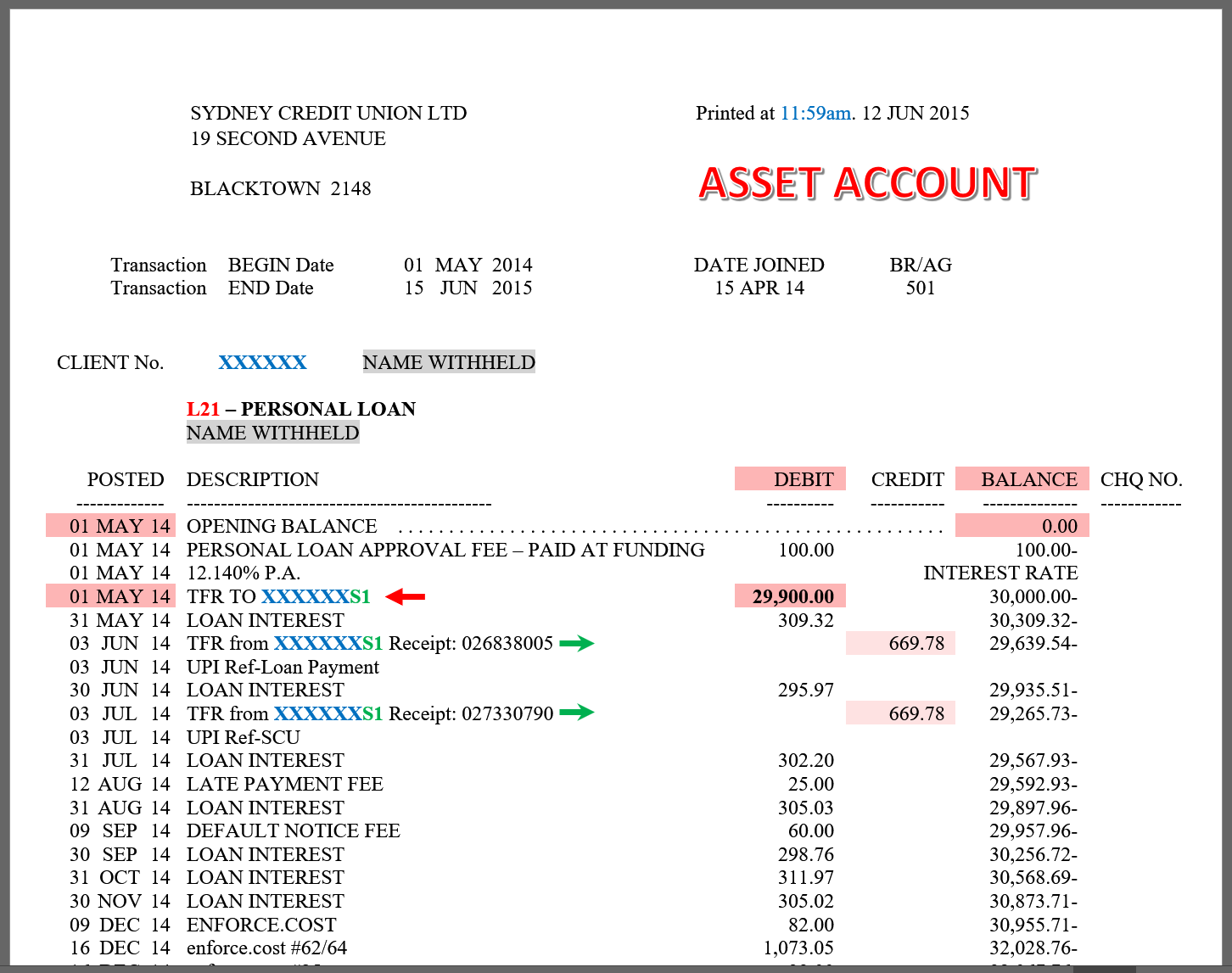

In Figure 3, each Debit-item increases the Balance, first from 0.00 to 100.00-, then to 30,000.00- (with minus signs ‘-’ after balance numbers). These facts confirm they are Debit-balances [RULE 4a]. By RULE 3, this is the SCU Asset a/c.

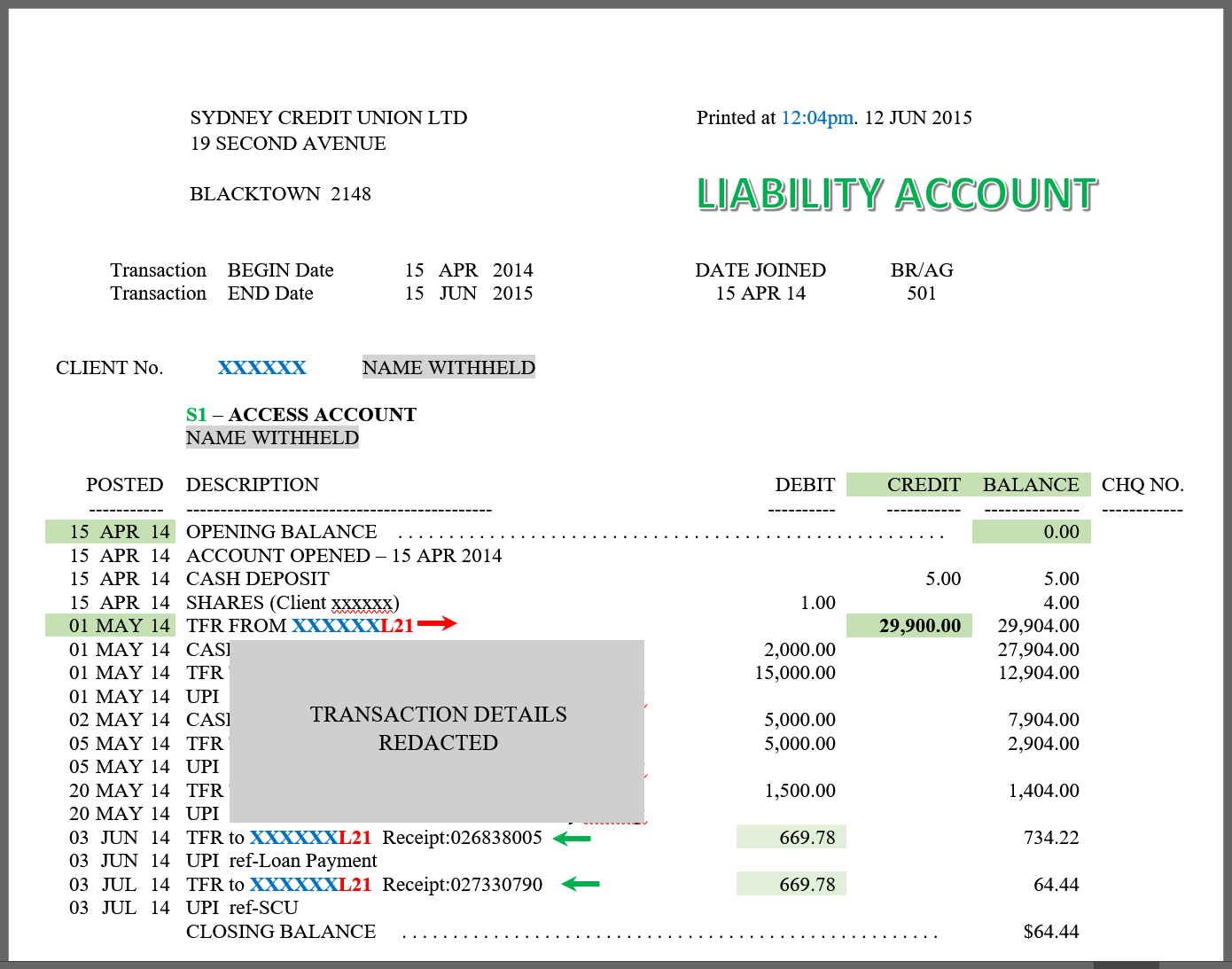

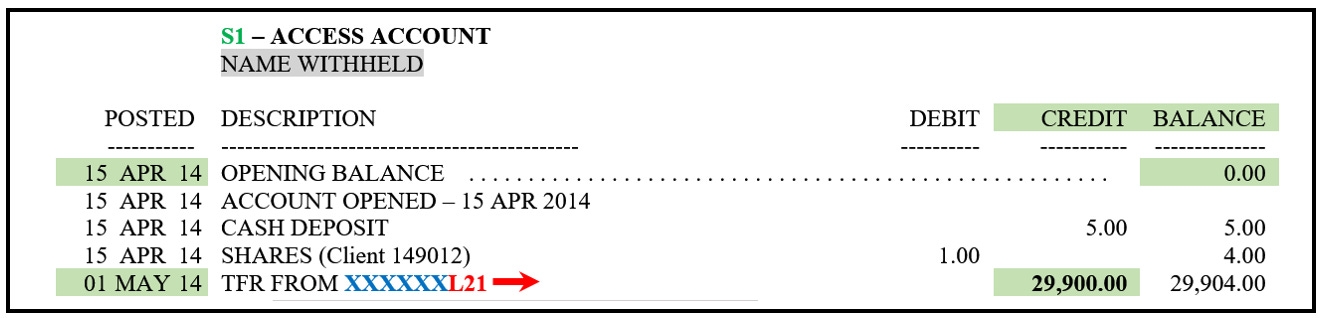

Similarly, in Figure 4, each Credit-item increases the Balance, proving they are Credit-balances [RULE 5a]. By RULE 3, this is the SCU Liability a/c. Tony’s new loan of “29,900.00” (green) appears under the heading “CREDIT” (green) on “01 May [20]14”.

Although Tony’s CLIENT No XXXXXX appears in the “Description” column three times, I’ll omit it in discussion and just use the account codes, “L21” and “S1” for the Asset and Liability a/cs, respectively. I’ve also added red and green arrows to Figures 3 & 4 to show the meaning of codes beginning with “TFR”, an obvious abbreviation of “Transfer”.

The arrow directions point TO-wards or away FROM the “[a/c no] XXX …”, as the codes describe.

The arrow colours match the colours of the alleged fund “source”, i.e., the accounts FROM which the funds are “transferred”, as the codes describe.

Take a moment to look back at Figures 3 & 4. Take your time and absorb what those codes (words?) and arrows are telling you because, in the red-arrowed transactions, there is magical deception afoot.

Preliminary Observation

Unlike the previous case with the ANZ Bank, there is no problem with RULE 2 here. The central columns in these two accounts are both correctly labelled, with “Debit” on the LH column and “Credit” on the RH column.

Forensic Examination

Errors in the SCU Asset a/c

Though any error in accounting is bad practice, I’m going to down-play these first two errors in this L21 asset a/c as relatively venial sins because they don’t play a significant role in my analysis of the fraudulent aspect of these accounts.3

1a. Timing & Description Errors

The first error is that the top two Debit-items in Figure 3 (and Figure 5, below) record two deposits in the wrong order [viz., first the $100.00 & then the $29,900.00] totaling 30,000.00 on 01 May 14 when, logically, the first item should come after the second item. The first deposit made that day was Tony’s signed “loan agreement”, treated as a negotiable instrument with commercial value of $30,000.00. As neither of those items is a true record of what was deposited by Tony, I regard them as two separate errors and two false transaction descriptions.

1b. “Matching Principle” Violation

Next, the 100.00 Debit-item has no matching 100.00 Credit-item anywhere, breaching the matching principle. That unmatched item can’t represent payment of the Loan Approval Fee by Tony out of his loan funds in the Liability a/c. That would be shown as (i) a 100.00 Debit in the Liability a/c (green) - showing Tony’s withdrawal from “his funds” and (ii) a 100.00 Credit in the Asset a/c (red). So there is no proper record of “Tony’s payment” of the fee in the accounting record.4

If these errors were corrected, the accounts would show:

first, a 30,000.00 Debit-item in the Asset a/c, recording the deposit of Tony’s signed “loan agreement”, and a matching 30,000.00 Credit-item in the Liability a/c, giving Tony a Credit-balance of 30,004.00 in the Liability a/c; and

only then could the $100 “Fee” have been debited from that 30,004.00 Credit-balance in the Liability a/c and credited to the Asset a/c, giving a full accounting record of the fee payment by Tony from his “loan funds”, leaving the 29,904.00 Credit-balance shown in the Liability a/c.

For simplicity, I’ll ignore these errors in following discussions of the ‘mortal sins’ related to the “credit-creation” issue I’ve been highlighting.

2. “The Grand Illusion” in the Asset Account L21

In this case, the fraudulent “errors” are in the innocuous-looking Description with the red arrow on 01 May 14 in Figure 3, which I’ve extracted and reproduced in Figure 5 (below), viz., “TFR TO … S1 … 29,900.00”, with that number in the (LH) Debit column.

Think carefully here. You are being told in that single line that this highlighted 29,900.00 Debit-item (red) is moving out of this L21 account and going into the other [S1] account, as though the word “Debit” means “Withdrawal”.

That description “TFR TO … S1 … 29,900.00” is effectively alleging a “withdrawal” of $29,900 from an asset account which, at that moment, contained a mere $100.00 [the fee paid by Tony]!

Wouldn’t you like to be able to withdraw $29,900.00 from your bank account when the balance was only $100.00?5

Does any of that ring a bell? Have you seen something like that before? Is the message getting through? If you look back at our set of rules, because the “29,900.00” is in the LH Debit column, RULE 4a tells us that it represents the deposit of an asset worth $29,900.00 into this Asset a/c L21, increasing the Debit-balance from “100.00-” to “30,000.00-”, and NOT a withdrawal.

This red-arrowed description is an accounting LIE.

If the Truth was located in the North on a map, this description is pointing you towards the South.

This L21 a/c was not “empty” at that moment, but its “100.00-” Debit-balance at that time would not support an out-going transfer of even “100.01”, let alone a “29,900.00” transfer. IF there had actually been a ‘29,900.00 transfer’ from L21 to S1 (which there wasn’t) that would have been a fraudulent breach of Rule 0. But there is no breach of Rule 0 here, because there was no “out-going transfer”.

The Illusion

See how the deception works? The words associated with the number ‘29,900.00’ contradict the accounting implication of the placement of the number ‘29,900.00’?!

It’s quite subtle magic, but magic nevertheless. By falsely describing an ‘in-coming deposit’ [i.e., a debit-item in an asset a/c] as an ‘out-going transfer’, the reality of that deposit is inverted.

Here we see “The Grand Illusion” again, as previously described in article #2 about the ANZ Bank. The description “TFR TO … S1” is the SCU version of “ABRACADABRA”. These false [code] words written on this a/c statement directly contradict the accounting reality represented by the position of the number “29,900.00” in the LH or Debit-column on the same document.

The description “TFR TO … S1” is the SCU version of “ABRACADABRA”

Tony’s very real “30,000.00” deposit into the Asset a/c has simply ‘disappeared’.

In its place, ‘transformed’ by the magician’s narrative (a magical word-spell), is an alleged, but impossible, “29,900.00” funds transfer out of that Asset a/c.

That coded transaction Description, “TFR TO … S1”, is not simply incorrect, it’s very misleading and (I say) fraudulently deceptive.

Could a competent accountant make such a fundamental mistake as to call an “in--coming deposit of $29,900.00” an “out-going transfer of $29,900.00”? I doubt it. Or does that accountant really believe s/he can withdraw 29,900 eggs from a basket containing only 100 eggs?

Two evident facts on the face of this account prove the description is false, because IF it were indeed an out-going “Transfer [from L21] to S1”, as described:

It would be treated as a “withdrawal from” L21 and recorded in the RH Credit-column, not the LH Debit-column, in that a/c; and

It would then be in breach of RULE 0 and a simple fraud. It is simple fraud to attempt to withdraw (or transfer) a $29,900.00 asset from an account containing total assets of only $100.00.

Could these deceptive descriptions just be honest, silly, one-off ‘descriptive’ mistakes? Again, I’ll defer answering that here. Let’s first see what we find in the Liability account S1 (see Figure 6 below).

3. “The Grand Illusion” in the Liability Account S1

My assessment of the above Asset a/c ‘error’ is confirmed and the false Description in the Asset a/c (above) is reinforced in Line 5 of the Liability a/c, in the red-arrowed transaction description recorded on 01 May 14, viz., “TFR FROM … L21 … 29,900.00”, with that number positioned in the RH (Credit) column.

Having already described and discussed this “Grand Illusion” in my previous article at some length, I won’t repeat that here.

It should be clear now that this 29,900.00 Credit-item (green) in the S1 Liability account (Figure 6, above) is not the result of a fictitious “Transfer from … L21”, but actually the matching entry for the equal 29,900.00 Debit-item on the same day (01 May 14) in the L21 Asset account, in Figure 5, above.

By now I hope you are starting to get the feel of what a “double-entry” is, how it serves to keep the accounting equation in balance, and why accounting has this “matching principle” as its foundation. That transaction was a deposit by Tony of a “negotiable instrument” with real commercial value of $30,000.006. In D-E accounting, a pair of “matching items” (like these two red-arrowed items) is the minimum required to record the TWO obligations arising from such a transaction, viz.,:

The Credit Union’s obligation to pay the loan to Tony (the Credit-item in their Liability a/c); and

Tony’s obligation to repay the loan (the Debit-item in their Asset a/c).

Those matching items do NOT represent two different transactions but two aspects of the acceptance of Tony’s “loan agreement” by the Credit Union as a negotiable instrument worth $30,000.00.

Each item complements the other;

Each item is a necessary part of the record of a single transaction; and

Either item, alone, is incomplete.

What is this “mysterious” TRANSFER transaction”?

So, the false Description, “TFR FROM … L21” in Figure 6, again raises the same questions about the competence (or honesty) of the SCU accountant, because we have already concluded above that there was no outgoing transfer FROM the L21 Asset account. This makes the “Description” - implying an in-coming “transfer” from the L21 Asset account - equally incorrect, as well.

Both of these red-arrowed Descriptions are creating the same false impression as we saw in the previous article on the ANZ Bank case, viz. that a transfer of funds occurred from the Asset account to the Liability account, when no ‘funds’ are actually “moving” anywhere or at all.7 The transaction being recorded by this pair of items was the “acceptance of Tony’s ‘promissory-note’ by the SCU”. They record the dual effects of the agreement reached between Tony and the SCU.

In the previous article, I called this deception “The Grand Illusion”, and here it is again, in slightly different clothing, but still recognizable.

See my previous article (#2) about the ANZ Bank for a detailed description of the entries that such an alleged “transfer of funds” would leave in the Credit Union’s accounts. Suffice to say here, such an alleged transfer is impossible, and if attempted in practice, would result in the most bizarre outcome for the customer.

The Deception

To recapitulate briefly,

A magical illusion has been created.

These false descriptions lead a gullible customer to believe (mistakenly) that $29,900.00 worth of “funds” were initially owned by the SCU, were somehow stored in their ‘empty’ L21 Asset a/c, and came out of that L21 Asset a/c as a “loan of credit”, which was “transferred from” their L21 Asset a/c and “deposited” into their S1 Liability a/c.

This is a magical deception. This is what “credit-creation” or “creating deposits” really looks like in the false accounting language of “lending” institutions in Australia.

The SCU confidently states that it can pull a $29,900.00 “rabbit” out of it’s practically empty “Asset Hat” in front of your eyes.

It has created a false narrative, a fictional story, which suggests that it has withdrawn $29,900.00 of “Credit” from its L21 asset a/c and “deposited” it in its S1 Liability a/c.

By wrapping those deceptively false words around the correctly positioned number on the account, they falsely claim ownership of Tony’s $30,000 asset (represented by the Debit-balance in the Credit Union’s Asset a/) in order to “lend” his Credit-balance back to him.

If you hadn’t already noticed, this magical Credit-item of ‘29,900.00’ appearing in Tony’s account (a.k.a. the Credit Union’s Liability a/c) is no different from an ordinary Credit-item he would see if he deposited $30,000 in cash (from which $100.00 was to be deducted as a Fee). He owns this magical Credit-item in exactly the same way as he would own that ordinary one.

Clearly, the Credit Union can’t lend Tony what he already owns, as creditor!!

The Reality

On 01 May 14, the SCU Asset a/c (L21) was empty: “Opening Balance … 0.00”.

The accounting facts recorded are:

the 30,000.00 Debit-balance in the L21 Asset a/c records the commercial value of the “loan agreement” deposited by Tony at the SCU, promising to pay both a $100 fee and a $29,900 ‘loan’; and

the 29,900.00 Credit-item in the S1 Liability a/c, records the obligation of the SCU to pay Tony the balance of the promised loan money (after deducting their $100 fee).

That SCU-debt of $29,900.00 belongs to Tony, as CREDITOR. Tony became a Creditor at the instant the SCU accepted his signed loan agreement. From that moment on, the SCU was, and remained, the DEBTOR on that Liability a/c, and nobody can lend their own liability. Or, to put it the other way around, the SCU can’t lend a person something he already owns, as CREDITOR.

The 29,900.00 Credit-item was Tony’s asset as soon as it appeared in that account, and this fact was being hidden from him (and the court, in this case).

See the “trick”; shatter the illusion!

As noted in the previous case with the ANZ Bank, remember the magician’s misdirection technique.

What’s different about the Green Arrows?

In Figures 3 & 4, I’ve placed green arrows against four items, two in L21 and two in S1, on the dates 03 JUN & 03 JUL. Although the corresponding “TFR to” and “TFR from” Descriptions seem very similar to the false descriptions marked with red arrows (discussed above), the direction of the green arrows in each a/c is opposite to the direction of the red arrow above them. It’s also clear that each of these items refers to a “Loan Payment” by Tony of $669.78 out of his funds in the Liability a/c.

It is perfectly proper for Tony to withdraw his funds from his Credit-balance in the Liability a/c and deposit them into the Asset a/c, to reduce the Debit-balance representing his liability to the SCU. That process is actually a “Transfer” and that is what each pair of “669.78” Debit- and “669.78” Credit-items represents.

For each “Loan Payment” item in the S1 Liability a/c, the preceding Balance was sufficient to support Tony’s $669.78 withdrawal from his credit-balance; each $669.78 item is correctly recorded twice: (i) as a Debit-item, reducing the previous Credit-balance in the Liability a/c [RULE 4b]; and, (ii) as a matching Credit-item, reducing the previous Debit-balance in the Asset a/c [RULE 5b]. In accounting terms, the green-arrowed items are both correctly entered and correctly described.

But the red-arrowed items are both incorrectly entered (wrong column for the description), and incorrectly described (as transfer from L21 to S1). In each case both red-arrowed items are false, misleading and deceptive.

Proof of this claim? Examine the Balances immediately before each arrowed item. Look again at Figures 3 & 5 to see that the L21 account Balance immediately before the 29,900.00 Debit-item was “100.00-”, completely inadequate to support the alleged outgoing transfer of 29,900.00 (which was in the wrong column, as well). Nobody can “withdraw” 29,900 ‘eggs’ from a box containing only 100 ‘eggs’.

But even that “alleged outgoing transfer” proved to be the result of a false description, since the amount was posted as a Debit-item in an Asset account, meaning it was a deposit into, not a transfer out of that Asset a/c.

Summary

Summarizing the above forensic examination, these account statements show conclusively that:

Before any transactions occurred on 01 May 14, the Asset account L21 was empty (see Figures 3 & 5; “OPENING BALANCE … 0.00”);

When the 29,900.00 Debit transaction occurred on 01 May 14, the Asset account L21 had a Debit-balance of “100.00-” (allegedly due to receipt of the “$100.00 Personal Loan Approval Fee”), so low as to make such an alleged ‘outgoing transfer’ [if attempted] a breach of RULE 0 and an attempted fraud;

No funds were ‘transferred out of’ that account on 01 May 14, as there was no Credit-item entered in the Asset account L21 until 03 June 14; and

Therefore, the 29,900.00 transaction, entered as a Debit-item in the Asset account L21 on 01 May 14, was due to the receipt of a new asset worth $29,900.00. This asset can only be the remaining commercial value of Tony’s $30,000.00 Loan Agreement after deducting a “$100.00 Personal Loan Approval Fee”.8

I wonder how a judge would treat a “lender” if such false entries, visible on the face of their accounting records, had been pointed out in evidence in a court hearing?

Again, I’m postponing detailed discussion of the implications of the evidence I’m presenting here. Feel free to comment about those implications, as you see it, based on the evidence you have seen so far.

I have one more set of accounts to go. Don’t miss it by failing to make your free subscription.

I do look forward to your comments. And I want you to call out any errors you see. If I am wrong, please show me the error and explain what is wrong.

If you like what you’ve seen here so far, please share it. The more people who understand what “lenders” are actually doing, the sooner we regain a correct relationship with them and with our credit (i.e. as Creditors).

I’m not charging for access to this information but your free subscriptions do give me useful feedback and as a free subscriber you won’t miss future revelations about another bank.

Following a series of mergers, most recently in 2018, SCU is now named Australian Mutual Bank Ltd.

This article will not discuss the cause, outcome or merits of Tony’s legal case.

I include them to avoid accusations of doing an ‘incomplete’ analysis.

The matching principle has been breached because the (green) loan item of 29,900.00 Credit (in the Liability a/c) does not match the sum of the 100.00 and 29,900.00 Debits (in the Asset a/c).

If you tried that you could be charged with attempted fraud.

Such “signed loan documents” can be, and are often, sold for cash by these institutions without the knowledge of the customer.

Simultaneously debiting the Asset a/c and crediting the Liability a/c with the same amount (29,900.00) does NOT represent a “transfer” of 29,900.00 from the Asset a/c to the Liability a/c. Such an hypothetical “transfer” in that direction would require a Credit in the Asset a/c (representing a “withdrawal”) and Debit in the Liability a/c (representing a “reduction” of the SCU liabilities), the exact opposite of what we see here. By that “transfer”, both the assets and liabilities of the SCU would be reduced by the same amount (keeping the ‘accounting equation’ in balance) and there would be no “loan” funds available as a “credit-balance”.

See earlier discussion of “Description Errors”, about the false description of Tony’s initial $30,000.00 deposit.

i always wondered how the banks [1] make money out of thin air, then [2] proceed to make us feel like we are indebted to them for this magic.

you are showing me how they do this with their magic double entry book keeping 'entries.'