#5 - More Evidence: Rural Bank accounts; deconstructed

More banking magic - Elders Rural Bank 2006 (~12 minute read)

More evidence of accounting fraud by lending institutions in Australia

You might think two unrelated Australian banks behaving badly (see articles #2 and #3) were a mere coincidence, or two statistical outliers, not evidence of systemic corruption.

So here’s a third case - and my six rules of accounting haven’t changed1.

The EVIDENCE

This case dates from 2006 at Elders Rural Bank2 and I’ll call the customer “Tim”.

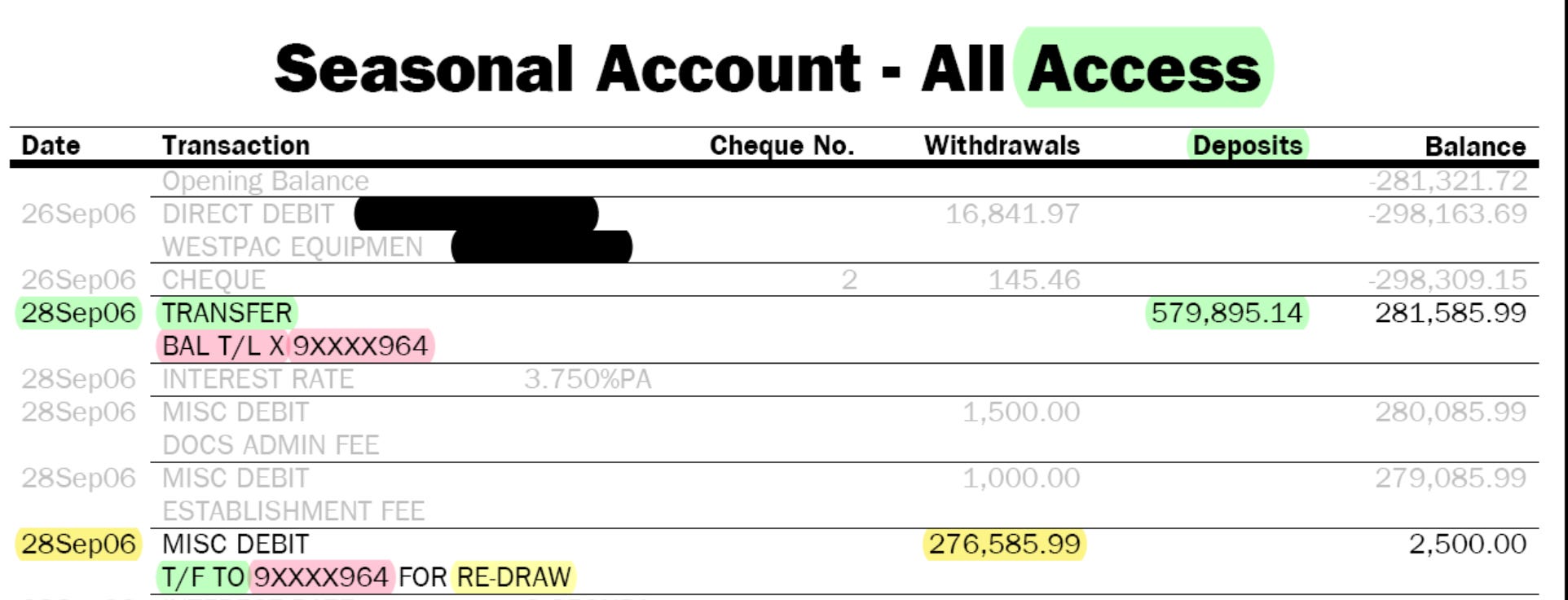

Tim, who was switching banks - moving from Westpac to Rural Bank - was granted a loan of $800,000.00 to pay out Westpac’s mortgage and fund his ongoing business. Figure 13 shows his documents with name & address redacted and account numbers partly redacted to ensure accuracy but maintain privacy.

The LH panel In Figure 1 shows Statement Number 001 of the Term Loan a/c No. 9xxxx964 with the two debit entries originating his $800,000.00 loan on 28 Sep 06.

The RH panel shows Statement Number 051 for the matching period for the Seasonal account - All Access a/c No. 3xxxxx078, which has an “Approved Overdraft Limit” of $100,000.00, shown in the box “Your details at a glance”.

My Colour Code

I’ve used different colours to highlight key items in the asset a/c (pink) and liability a/c (green). The third colour (yellow) I’ll explain later.

The Asset account (Figure 2, below) shows a zero “Opening Balance”, two pink “Drawdowns” and a yellow Transfer.

The Liability account (Figures 3, below) shows a green “Transfer” - matching the second pink “Drawdown” (above) - and a yellow Withdrawal resulting in the yellow Transfer, above.

Forensic Examination

In this case, what I’m calling the liability a/c has an “Approved Overdraft Limit”, so it shows balances with and without a minus sign [‘-’], meaning it can be either an asset a/c (when overdrawn, showing ‘-’ sign) or a liability a/c (when not overdrawn). You can check the current status of the a/c on a given date by noticing whether or not there is a ‘-’ sign in the current balance4.

Outline of Evidence - Red Flags

Those who have followed my previous “Deconstruction” articles will have already spotted three red flags, namely, use of incorrect column headings and misuse of the terms “DRAW DOWN” and “TRANSFER”, all of which we’ve seen previously.

1. Column Headings

Only the LH column in the asset a/c is correctly headed “Debits”. The RH column label, “Payments”, is ambiguous: it could mean either incoming or outgoing.

In the Liability a/c, “Withdrawals” and “Deposits” are suspicious.

2. “DRAW DOWNS” in Bank Asset a/c

Figure 2 shows two debit-items (pink) on 28Sep06, each with the description “DRAW DOWN” - one to “REFINANCE WESTPAC”, the second described as a “T/F TO” [transfer to] the Access a/c “3xxxxx078” - together amounting to “800,000.00”, the amount of Tim’s “loan”.

But neither of these items is, or can be, a draw-down (i.e., withdrawal) because (a) if they were, they’d both be in the RH (Credits) column and (b) this account was empty when they were recorded, as shown by the “Opening Balance” of “0.00” immediately above them.

3. “TRANSFER” between Asset and Liability a/cs

The ‘DRAW DOWN” of “579,895.14” [pink debit-item, Figure 2], matches the “579,895.14” in the Liability a/c [green credit-item, Figure 3].

As previously, the labels on this pair of matching entries FALSELY describe a “TRANSFER” of funds FROM the asset a/c TO the liability a/c under the column heading “Deposits”.

There are three problems here: (a) this RH Credits column label (“Deposits”), breaches RULE 2, (b) nothing was “deposited” in this liability account, and (c) this (green) “Transfer” was NOT a transfer.

We’ve seen all these “errors” before but I’ll analyze them again, very briefly.

“ERRORS” in Asset a/c

1. False Transaction Description

The first transaction on 28 Sep 2006 was Tim’s DEPOSIT of his signed “Loan Agreement”, a note with commercial value of $800,000.00. Not describing that huge transaction truthfully is bad enough. At the very least that’s false accounting.

But recording it as its opposite, viz., two WITHDRAWALS (i.e. “DRAW DOWNS”) totaling $800,000.00 is a blatant lie which reverses the nature of the transaction.

2. Column Headings contradict Transaction Descriptions

As with the ANZ Bank, by placing alleged “DRAW DOWN” items in the LH Debits column, the bank identifies them as Deposits rather than Withdrawals (or “Draw downs”) - which should be placed in the RH column in an Asset a/c. This is basic rule-breaking. The attempt at deception should be obvious to anyone familiar with the rules of accounting.

A true “DRAW DOWN” should decrease the debit-balance of the Asset a/c. These a/c balance increases and their contradiction of the transaction description, should stand out like the the proverbial bull’s ‘tentacles’.

3. [apparently] Breaking RULE 0

Yet another problem with both of these entries is the same as we saw with the ANZ Bank in article #2, namely, each is described as a “DRAW DOWN” from an empty account. It was empty on “31Aug06” and remained empty [Balance = “0.00”] up to the moment these two “DRAW DOWN” items were posted on “28Sep06”. Under RULE 0, no funds can be withdrawn from an empty account, and attempting to do so would be a criminal fraud. While ‘pretending to’ is not criminal, why tell the lie?

Now you may suffer cognitive dissonance, because what are DESCRIBED as “draw downs” AREN’T (draw downs, that is), and there aren’t TWO of them; there was only one transaction and it was a deposit, so why do the numbers show two deposits in the LH (Debits) column?

This description of a “single deposit” as two “draw downs” is doubly fraudulent.

The magician has invited the ‘audience’ to form a false impression, viz., that “two separate amounts were being withdrawn from the empty Bank Asset a/c”, when no such “DRAW DOWN” did or could occur.

The impossible has been described as though it were the truth!

Two very valuable “rabbits” [combined worth $800,000.00] seem to have been pulled from the same empty “Asset Hat”.

If you don’t know the Rules regarding addition and subtraction in both types of account [RULES 4 & 5], the resulting illusion is quite hard to resist.

As I’ve said several times before, the magician’s WORDS contradict what the NUMBERS show us. So, believe their numbers, NOT their lying words.

And this is as far as I need to go with this Asset account. Once the above false “DRAW DOWN” statements have been recorded in the Asset a/c, “The Grand Illusion” is in effect and subsequent entries can (and will) follow the ordinary rules of Double-Entry accounting.

“ERRORS” in Liability a/c

1. The Impossible “Transfer”

The Transaction descriptions for the two matching “579,895.14” items in Figure 2 and Figure 3 begin with the words “DRAW DOWN” in the Asset a/c, and “TRANSFER” in the Liability a/c.

The bank is telling a ‘story’ here, to the effect that there was a $579,895.14 out-going “DRAW DOWN” from the Asset a/c 9xxxx964 and a $579,895.14 in-coming “TRANSFER” to the Liability a/c 3xxxxx078.

As explained previously5, this alleged DRAW DOWN from a/c No. 9xxxx964 for TRANSFER to a/c No. 3xxxxx078:

did not happen, as described; and

could not have happened, as described; and

if done as described, would have left a very different numerical record from what appears in these accounts.

The above types of “Asset a/c errors” we’ve seen before, but there’s another error we’ve not seen in previous accounts.

2. Account Concealment

In Figure 3, the bank posted a “579,895.14” Credit-item to match the second “579,895.14 DRAW DOWN” Debit-item in Figure 2, but did NOT post a “220,104.86” Credit-item matching the first Debit-item: “220,104.86 DRAW DOWN”.

That missing “220,104.86” Credit-item must exist under the matching principle and, as it is part of Tim’s loan, it should appear as a credit in an account bearing his name. But no such Credit-item has ever been seen. If it exists, it has been concealed from Tim.

One thing is certain: the Bank did not withdraw (i.e., credit) $220,104.86 of its own funds from its Cash-asset a/c to settle Tim’s $220,104.86 Westpac mortgage. No bank is ever going to pay out its own assets, when it can use the customer’s “borrowed funds” instead!

What Truthful Accounting would show

If the above “errors” were corrected, these accounts would show:

a single $800,000 Deposit, recorded as a Debit-item in the Asset a/c. It would properly be described as something like “commercial value of Loan Agreement”;

a matching $800,000 Credit-item in the bank’s Liability a/c, would record the funds owed to Tim under the agreement, and be followed immediately by;

a $220,104.86 Debit-item in the bank’s Liability a/c (Tim’s Access a/c), recording the withdrawal of portion of Tim’s funds from the Liability a/c for transfer to Westpac to settle his previous mortgage.

The Magical Fraud, again

These items raise the same issues as the red-arrowed items in the Sydney Credit Union accounts in article #3 regarding the Sydney Credit Union.

As explained at length in two previous articles, these identical numbers - a Debit in the Asset a/c and a matching Credit in the Liability a/c - do not represent a combined ‘draw down’ and ‘transfer’ process, but are the Matching Entries required to describe a single Deposit transaction.

In this case, the reality of that single Deposit of an $800,000 asset has magically ‘disappeared’.

In its place are two debit-items, fraudulently described as ‘Draw Downs’, to Tim’s enormous detriment and the equivalent advantage of the Bank. Tim willingly gave up his $800,000 asset and the bank took possession of it with no price paid.

I say the bank paid nothing to acquire that $800,000 asset because, what the bank offered Tim in exchange for it was a “written record of the amount they should pay” him, but do not pay. Instead, they give him a “bank IOU”. That magical “transformation” amounts to a criminal change-of-ownership of an $800,000 asset, otherwise called “theft”.

What actually happened on 28Sep06?

Magic!

The text descriptions of the two Debit entries totaling $800,000.00 in the Asset a/c imply that two separate withdrawals were made by the bank on the 28 Sep 06.

That is a false illusion. On that date, these accounts show NO withdrawals; only a false description of the deposit of an asset valued at $800,000.00, viz., Tim’s signed “loan agreement”.

This apparent splitting of one actual Deposit (by Tim) into two mythical “DRAW DOWNS” (by the Bank) is the magician creating the illusion of “multiple withdrawals”, where no withdrawals actually occurred. More importantly, the Real magic is the implied change of ownership: the ‘transformation’ of Tim’s real Deposit of $800,000 into the Bank’s mythical “Draw Down” of $800,000.

Do you see the parallels and similarities with my two previous “Deconstructed” articles? Are you beginning to see a pattern? Can you see how the crime is being committed now?

Falsely describing a single Deposit as two separate DRAW DOWNS (from an empty a/c) is not a simple boo-boo, a slip of the pen, an accidental error; it is a series of carefully constructed false statements designed to misdirect the attention of the customer (and bank regulators).

This is “ABRACADABRA” dressed in an accountant’s garb(age).

This is the ugly reality of bank “credit creation”.

And, as repeated several times in previous articles, and as this Bank of England article reinforces, the Credit-balance, which was created, belonged to Tim, as CREDITOR. The bank cannot lend Tim what he already owns, as Creditor!

See the trick! Explode the illusion!

What about the Yellow “Transfer” in Figure 2?

Oh yes, I almost forgot about the yellow “Transfer” item in the Loan account in Figure 2. Why do I complain about the pink “Transfer” and not the yellow one?

Because the yellow one - a withdrawal from the Access a/c - is REAL while the pink ones are both FAKE - pretending to be “withdrawals” from the empty “Loan” a/c.

What do I mean? I mean the yellow one is operating on a non-zero account Credit-balance in the Access (liability) a/c, whereas the two pink ones are operating on an empty Loan (asset) a/c (“Opening Balance = 0.00”).

On “28Sep06” the previous Credit-balance in the liability a/c was $279,085.99, so it’s OK to withdraw $276,585.99, leaving a Credit-balance of $2,500.00.

But when the previous Debit-balance in the asset a/c was $0.00, it’s NOT OK to pretend to withdraw $800,000.00! It is fraudulent pretence and actually criminal if done with foreknowledge and intent to deceive.

I choose to believe that bankers everywhere have the clear intention of benefiting themselves at their customer’s expense, and the physical evidence showing how they do this is now out in the open for all to see.

Now convince me this is “mere coincidence” and NOT criminal.

And so, “The Prosecution Rests”

Well, that concludes the “Case for the Prosecution”.

I’d like to hear any defence these corporations might like to produce and will happily consider publishing such, if any are forthcoming.

I will stipulate the usual reservation of rights:

to ‘cross-examine’ any witnesses presented;

to object to unfair tactics;

to remove disparaging comments; and

to rebut any new evidence they can present (which must be appropriately supported by sworn affidavits).

As always, please point out any errors you notice in a comment. If I am wrong, I’ll admit my mistake and correct the error.

Sharing is caring. If you know someone who could use this information, please feel free to share it with them.

From here on, I’ll probably focus on the consequences of what this evidence proves. We now have a new way of looking at ‘economics’, because we have a solid basis for making a very clear and necessary distinction between “credit” and “money”, the two forms of ‘exchange medium’ we all use almost every day without thinking too much about it.

If you’re interested in understanding how this changes the landscape of economics in general, then a free subscription would be the ideal way to follow, or participate in, coming discussions.

For an explanation of these Six Rules, refer back to article #1.

Subsequently called Rural Bank, but now A Division of Bendigo and Adelaide Bank Limited.

To emphasize relevant items in these documents, irrelevant text has been deliberately muted.

On “28Sep06”, the account was initially overdrawn, and the overdraft was cleared by the large credit-item arising from the deposit of Tim’s “loan agreement”.

See #3 - Sydney Credit Union Accounts; Deconstructed, s.3 and Footnote 7, and a longer explanation in #1 - Bank Accounting; Magic?

No doubt about it, there is some "creative accounting" going on in the banking sector!

It's no secret that banks are NOT lending out money they have in the vault, but simply creating credit out of thin air. Your articles are doing a great job of showing the sleight of hand that is used to obscure this fact.

However I am not convinced that Tim's promise to pay $800,000 really does have a commercial value of $800,000. To me it seems like the customer's flipside of the banker's scam - "Here is my promise to pay $800,000 (which I don't have), now give me the $800,000 that you just created".

Without the existence of the banking scam, Tim's promise to pay $800,000 would have much less value. If he approached an average citizen and requested $800,000 in hard currency, in exchange for an unsecured promissory note, he would not get very far - they would want an enormous discount for risk, or more likely, would place no value on it at all.

The only person who WOULD be interested would be a banker who has the ability to create $800 K from thin air, in exchange for a promise. The banker performed no exertion to "get" the $800K, so they can take a much greater risk in "lending".

The idea that "a man's word is his bond" is certainly appealing, and might apply amongst people who knew and trusted one another very well. However I don't believe that a man's financial promise is a commodity that trades at its face value, in a world where we have to deal with strangers as a normal part of life.

However I might be arguing against you AND the great Henry Hazlitt! I think he would take your side on this matter:

"There is a strange idea abroad, held by all monetary cranks, that credit is something a banker gives to a man. Credit, on the contrary, is something a man already has. He has it, perhaps, because he already has marketable assets of a greater cash value than the loan for which he is asking. Or he has it because his character and past record have earned it. He brings it into the bank with him. That is why the banker makes him the loan."